US large cap starting to get altitude sickness?

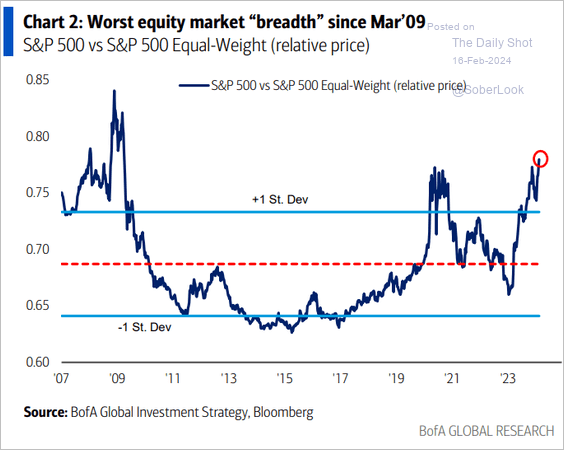

Traders are starting to bring back their expectations for the Federal Reserve to cut interest rates this year as there are signs that inflationary forces remain within the US economy. Following a slightly disappointing CPI report earlier in the week, Friday’s US producer prices, a measure of the change in prices that domestic producers receive for their goods and services, rose by more than expected from this time last year. US large-cap stocks fell marginally on the week, the NASDAQ tech index being the underperformer, as questions are being asked about how much longer this small band of merry stocks can continue to power on. Stocks in Europe had a better week, outperforming those across the water. One can see from the attached chart that the relative strength of these few stocks compared to the average stock in the index has reached extreme levels. Either the rest must play some catch-up, or big tech will face a setback.

Earnings season in the US is coming to a close as the vast majority of the S&P 500 have now reported. I think probably most of those names that draw the headlines, with possibly one exception. Top and bottom of earnings is that at the headline level, earnings grew yearly, according to Factset, by just over 3%, largely driven by tech and communication services.

As the prospect of Mr Starmer being placed into N010 at some point this year seems to grow ever stronger, it will be interesting to see how equity and bond markets prepare for such an eventuality. One could see bond yields rise as the market anticipates rising borrowing costs as concerns increase greater funding is needed to support its spending plans. Equities could suffer as overseas investors will not want to own assets in a currency that is likely to weaken. Although a weaker currency may help some larger-cap stocks profit as they derive a lot of their revenues from abroad. The UK stock market is one of the cheapest in the valuation of the developed economies, and that has not encouraged too many to dip their toes.

Looking to the week ahead, the one exception and probably the most anticipated of them all report this week is Nvidia—the supercharged stock offering the greatest exposure to the revolution of AI. The FOMC released the minutes of their previous meeting, which will be picked over looking for indications of the Fed’s thinking, at that point anyway, on rate cuts. Investors will also be drawn to the flash S&P Global PMIs, which are expected to show a small slowdown for both manufacturing and services. Berkshire Hathaway also reports earnings this week; any pearls of wisdom that drop from the great sage will be welcome. China reopens after a week-long Lunar New Year festivities. As for the UK, the CBI will release its industrial trends survey on Wednesday, which has not made great reading recently, and this one is unlikely to be much better. Markets in Europe are starting the week on the back foot.