There may be trouble but lets face the music and dance

Having spent the previous three months under something of a cloud, the sun shone on capital markets in November as all asset classes, with the exception of energy, had a pretty good month. The strongest performing sectors were tech naturally, financials, and consumer discretionary. Bond investors have not enjoyed much of the year, have had one of the best months for many a decade. Inflation rates falling around the globe faster than expected, along with a bag of mixed economic news has encouraged investors to believe the tightening cycle is over. At some point, possibly in the first half of 2024 interest rates will start to fall. As we enter 2024, much of the consensus seems to be that the US will avoid an economic recession, inflation rates will slowly drift to target and the Central banks will then slowly cut rates. Goldilocks is back in all her glory. The Fed has managed to engineer the perfect scenario.

US Consumer spending, inflation, and the employment markets have been cooling in November. Much of the economic data has come in below expectations reflected in the weakness of the Citi economic surprise index. Poor economic news has clearly been good stock market news. It would appear this newfound optimism could or should help support equities into the year-end, although a period of consolidation is probably in order. The level of optimism now enjoyed by equity markets is reflected in the Vix, which is trading right back to its historic lows.

Into the New Year, the debate will begin about how long can risk assets bask in the glory of weaker data in the hope that it will allow the Fed to cut rates. The consequence of falling inflation and the Fed remaining cautious to start cutting interest rates will result in a further rise in real rates, weakening growth.

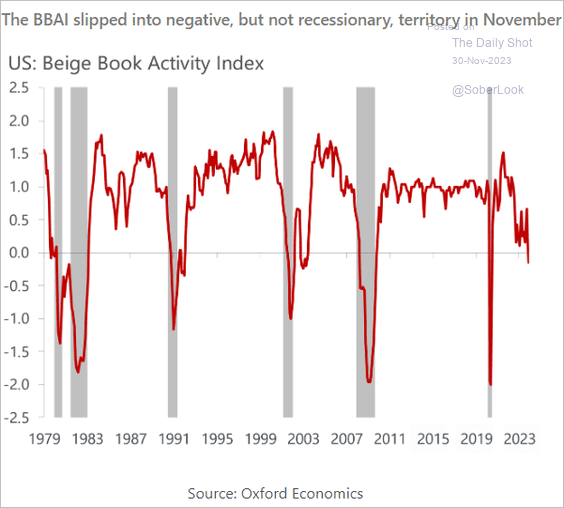

The latest Beige book survey combines reports from each Federal Reserve Bank bringing together the views on current economic conditions. The main conclusion from the report is that economic activity was softer, and the overall economic outlook has become less optimistic. The Oxford Economics Beige Book Activity Index dipped into negative territory for the first time since the COVID shock. Traditionally, when that happens as we can see by the attached chart courtesy of Oxford Economics the US economy contracts. John Authers points out the dramatic change in interest rate expectations that has taken place in the past month. Only a few weeks ago, the market predicted two rate cuts next year, and it is now baking in five. There may be a few clouds on the horizon.