Flowers need the rain to grow new buds

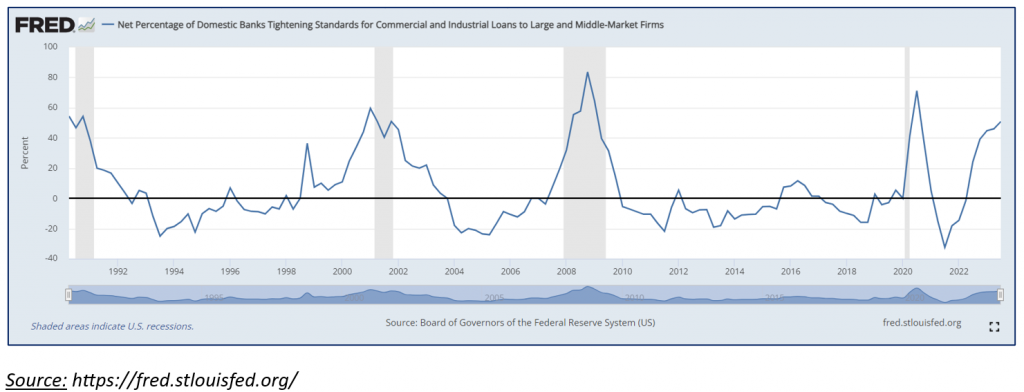

Bond yields creeping higher, as is the US dollar, hardly feels positive for stock market prices, as the S&P 500 feels like it is failing to break new ground. At present with much government debt offering 5% risk-free it feels hard to make a case for adding new investment into equities. Goldman Sachs yesterday offered a little ray of sunshine believing that there is only a 15% chance now of a US recession down from 20%. That feels a little optimistic as all the recent data indicates that the US economy is slowing down. In his Jackson Hole testimony last week, Jerome Powell referred to the tighter lending standards having an impact on the economy. With the chart attached, one can clearly see that as credit conditions tighten the economy slows, often causing an economic recession. The much-awaited ARM IPO failed to raise quite the valuation expected. Adding to the gloom, Klaas Knot, what a great name, Chairman of the Financial Stability Board told the G20 leaders that the economy is losing momentum and the effects of higher interest rates are starting to effect.

According to a Bloomberg report the consensus view for the earnings per share forecast next year for the S&P 500 is 246 dollars. At current levels that puts the S&P 500 on a forward multiple of 18x, which does include highly rated tech stocks, ex those, the forward multiple is probably closer to 16x. If the equity market derated to around 16x on economic slowdown fears you get to around 4000 for the S&P 500. If the economy slows and that earnings number becomes too optimistic by say 10% for want of a number, and the multiple is retained again you get to about 4000 for the S&P 500, just over 10% lower. One could paint a more pessimistic picture of the combination of lower earnings and lower multiples, we can leave you to do that maths on your own.

If all that seems a little gloomy, there is also no reason to get overly downbeat. Economic cycles are natural and occur on a regular basis. Downturns give an opportunity for some excesses to be flushed out of the system. They can give the opportunity for new investment. Leverage can be a wonderful thing, but at the wrong time can be brutally painful, forcing some to sell assets, but also giving others the chance to take on those assets, and borrowing costs will fall. One wonders if the Fed at least would welcome a mild recession, they would then be more comfortable that inflation rates would fall back to their target level and that would allow them to start cutting rates and supporting the next leg of growth.