Beauty is in the eye of the beholder

The big news of yesterday was the release of the latest UK employment data, which provided the Bank of England plenty of food for thought. Wages grew at 7.8% in the past three months, the fastest rate on record, according to the FT. As a result wages are growing faster than prices, which in theory should ease the much discussed “cost of living crisis”. Strong wage growth does not bode well for inflation falling back to the Bank of England’s 2% target anytime soon. Although there were signs that higher employment costs was starting to impact the jobs market as unemployment rose and hiring fell. What is also worth noting is 2 year gilt yields, considered the most sensitive to changes in interest rate sentiment, which a month ago were offering yields in excess of 5%, have fallen back down below 5%. There was little movement yesterday in UK government bond market to the employment report.

Generally equity markets feel a little stuck, the S&P 500 has gone up a bit, down a bit but is at the end of it all roughly where it was at the start of June, with on of the longest streaks recorded without a move of daily move of 2%. The US yield curve is roughly where it was a month ago. Today we get the latest US consumer price index for August. US Inflation is expected to rise to 3.6% from 3.2% in July, partially on the back of the recent rise in energy prices. The following day we get the latest US producer price inflation, which tracks the costs manufacturers pay to suppliers, likewise is expected to rise in August relative to July. The US dollar has crept higher in the past month, however commodity markets have likewise been largely treading water, aside from the oil price in the past few weeks.

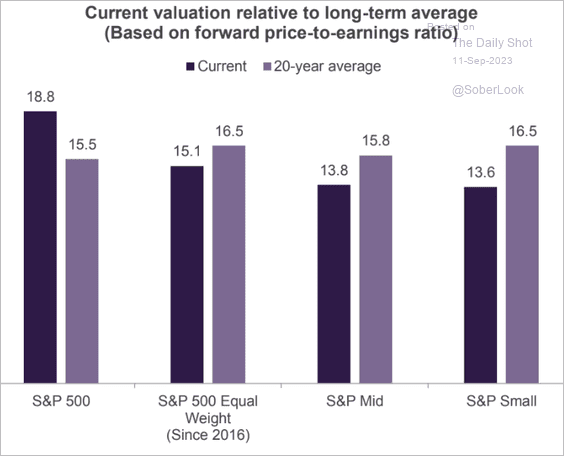

Much is made of the valuations in equity markets and I noticed the chart on the Daily Shot which illustrates that higher bond yields have had some impact on equity valuations as most markets look cheap relative to their 20 year averages. One can clearly see the real outlier is big tech valuations, skewing the S&P 500. The equal weighted index, admittedly only goes back to 2016, one can see is below its average. Small cap stocks look attractive based on this evidence.

The equal weighted S&P 500 earnings yield is around 6.5% (100/15), 10 year US treasury yields around 4.3%, equates to an equity risk premium of just over 2%. Not as attractive as it can be, but not as ugly as some would portray. The index is based on forward earnings expectaions which need to be met