Fear and Greed 2, Nvidia margins, just a few of my favourite things

We all read about or saw the employment data released yesterday; the long and short of it is that this report indicates the UK economy continues to muddle along. Public sector pay is still rising faster than in the private sector, but overall wage growth continues to slow. Retail and hospitality saw some of the strongest wage increases, as these sectors continue to feel pressure from the rise in the minimum wage; against today’s better-than-expected inflation report, wages are growing slightly ahead of prices. A combination of both report’s, the Bank of England will still not be in a hurry to raise interest rates.

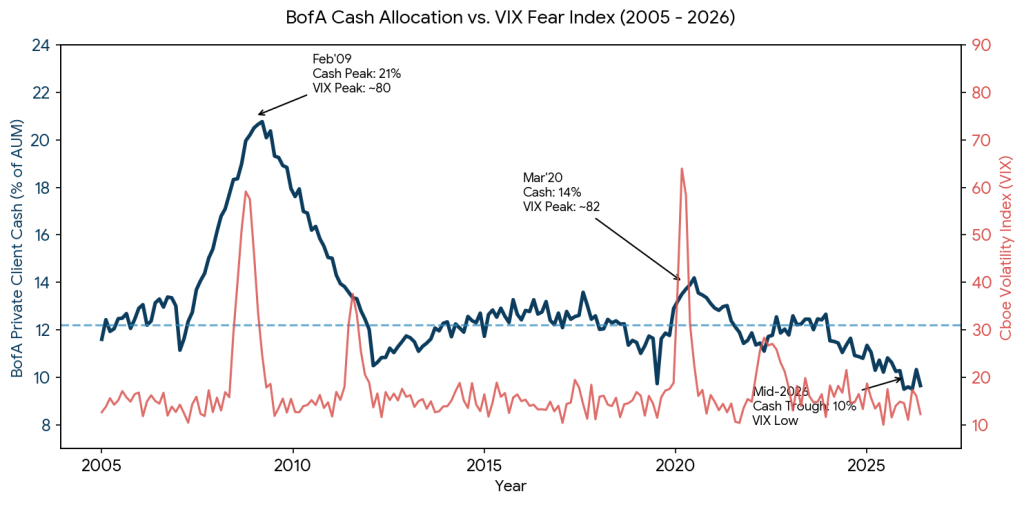

At the end of last week, I wrote a summary of some of the sentiment indicators I follow, particularly the fund manager surveys. Well, only yesterday I saw another handy chart, and one to give food for thought. This chart shows BofA clients’ cash holdings as a percentage of their AUM, pitched against the Vix index, courtesy of Daily Shot. One can see that just before the GFC, when the economic picture appeared rosy, cash levels were low, at the height of the bear market and fear in 2008, allocation was over 20% cash, and it was not until over 2 years later that they were back to their original investment level; in that time, the S&P 500 had gained 50%.

Again, look at 2019: as we approached COVID, cash levels were low; at the peak of COVID, they were high. Now, private client cash holdings as a percentage of the portfolio are about as low as they get. I don’t want those who read these blogs to think I am suggesting that one should rush for the door, but it is an alternative way of looking at fear and greed. Simply put, cash at its highest at peak fear, and vice versa

NVIDIA results are out later tonight. Consensus expectations are for revenues of $78.5-$79.2 billion, representing a year-over-year increase of approximately 78-80%, with an operating margin of approximately 60%, which is staggering. Particularly when you also consider that Nvidia is a manufacturing business, which, for a traditional manufacturer, is closer to 5-15%. Other semiconductor comparisons operating margins are closer to 35%; some are much lower than that. The market has forgotten how cyclical the semiconductor market can be, and even the greats like Nvidia, at some point, maybe years away, margins will narrow. Investors will take revenue for granted, margins will be the focus and drive the share price reaction tonight.

Longer-dated bond yields, not only in the UK but across the major developed markets, most notably Japan, the UK, the US and France, have been rising consistently since the start of the Iran conflict. Yesterday, the yield on 30-year Treasury bonds rose to 5.19% for the first time since June 2007:

Initially, stocks reacted in line with bond markets. Recently, there has been a divergence. Stocks have rallied and remained resilient, while bonds remain unloved. One or the other will change tack at some point; bonds have to rally, or stocks suffer.

One last thing, on BBC 2, there is a 3-part series on Elon Musk, worth a watch.