Hope against reality

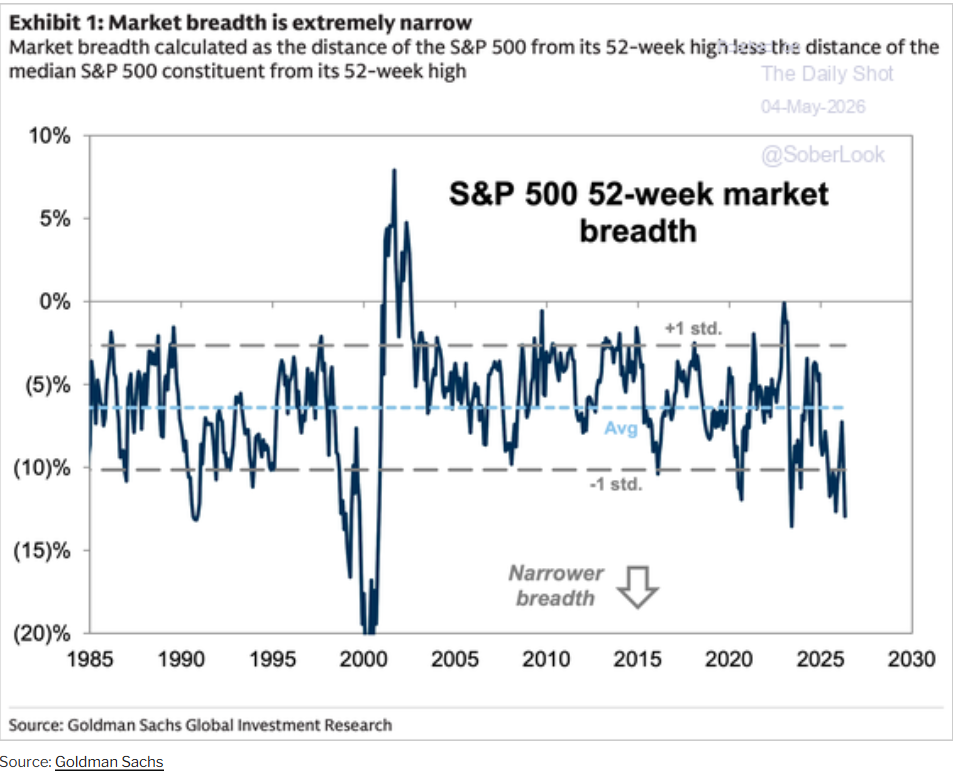

Some days it feels hard to know where to start. John Authers, this morning, highlights that owning quality stocks, those with strong balance sheets and steady profits, has been a losing strategy for investors ever since the tariff Liberation Day. Momentum stocks have driven the market to more record highs. I included a chart today, courtesy of the Daily Shot and Goldman Sachs, that clearly demonstrates how narrow the rally has become, and that a few stocks are once again propelling the S&P 500 to new highs. One can see from the chart what happened in 2000 as the dot-com bubble imploded, the speed at which momentum changes and how hard it is to adjust. Most investors, whether professional or amateur, tend to fish in the pond of quality. Makes sense, trouble is one can get sucked into following momentum. Investors talk about how expensive stock markets are, and as a headline, at the level that’s true, but it is also true that we have seen many quality stocks come back to valuations not seen in decades.

What does all this boil down to? What is driving all this? You don’t want to risk owning the Blackberry of tomorrow, just want to own the Apple. Own the AI winners not the losers. Also beware sentiment changes; it was not so long ago that the market had Alphabet as a loser in the AI race and Microsoft as the winner, but that sentiment has seemingly reversed. Some tech stocks that were ignored a few months ago, as the consensus view was they had little to offer the AI race, have now become darlings, and few own them, but are now being forced to bet one way or the other. History tells you quality wins through in the end.

Tomorrow we face the local elections, and if the pollsters are right, Labour are in for one hell of a beating as one Norwegian commentator described Norway’s victory over England in a 1981 football match. Kier Starmer will take the fall as his apparent opponents wait to take over. Will it be Rayner? Miliband, Burnham, the speculation is rife. Of course, he may just tough it out, he seems quite good at that. Bond markets seem to have sold off amid concerns that the government will need to borrow more, that inflation will pick up, that the weak economy will not generate the anticipated revenues, and that a change of leadership could make the situation worse.

When you buy a bond denominated in a foreign currency, you take on currency risk. No point buying a bond yielding 5% if the currency falls 5%, you make no money. So it’s interesting to note that the pound has remained remarkably resilient against both the euro and the USD in the past weeks despite the weakness in the bond market.